President Biden’s Medicare Shell Game

The White House’s budget proposals would improve the appearance of Medicare’s finances while disguising their actual deterioration

By Charles Blahous

In early March, the Biden White House released a fact sheet previewing his budget proposals for Medicare, advertised as dramatically extending program solvency without cutting any benefits or raising costs for its participants. But to call the proposals unhelpful would be a severe understatement. In reality, they amount to an accounting shell game: They would improve the appearance of Medicare’s troubled finances without meaningfully addressing the actual problem. The president’s framing also aims to extract political advantage from Medicare’s difficulties, positioning himself to attack any political opponent who tries to responsibly address Medicare’s runaway cost growth. The White House has rendered it prohibitively difficult for congressional leaders in either party to repair the situation at any time in the near future—and that’s a dynamic that can only undermine the public’s interest in a stable and secure Medicare program.

The Medicare Financing Challenge

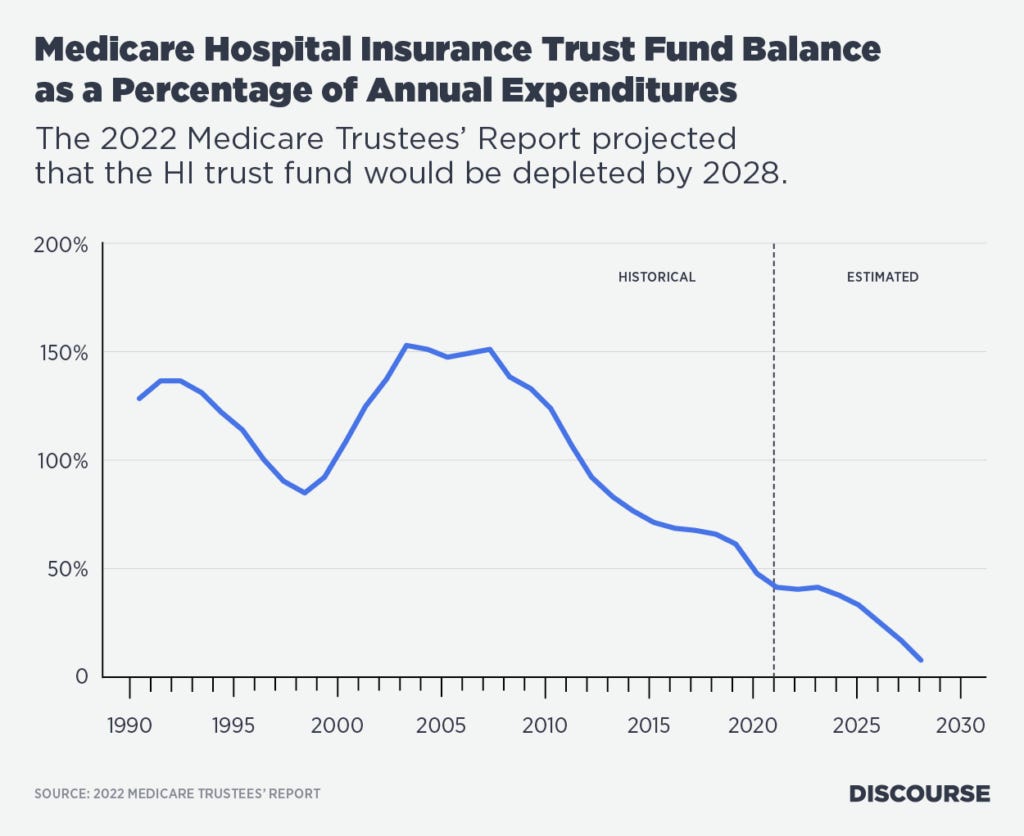

To understand the problems with the president’s proposal does not require an expert understanding of Medicare, but it does require familiarity with certain basics. First, Medicare provides different insurance packages financed from two separate trust funds: the Hospital Insurance (HI) trust fund and the Supplementary Medical Insurance (SMI) trust fund. The SMI trust fund is financed mostly by general government revenues, partially by premiums paid by (or on behalf of) beneficiaries, and to a lesser extent by other revenue sources. Medicare HI, however, is designed to be an earned benefit, funded by payroll taxes that workers pay from their employment earnings. For the HI system to work, the program must be kept solvent, meaning that its expenditures cannot exceed the amounts its tax collections can cover. One major current problem is that Medicare HI is going insolvent. Its costs are rising far faster than worker contributions can finance. Last year, its trustees projected that the HI trust fund would be depleted by 2028. At that point, it would only be able to make 90% of scheduled benefit payments.

Worrisome though HI’s problems are, HI is actually less than half of Medicare. Medicare SMI, which covers benefits such as physician services and prescription drugs, is larger and its costs are growing even faster. Medicare as a whole is growing far faster than our national economic output, an untenable situation requiring intervention by lawmakers to slow its cost growth.

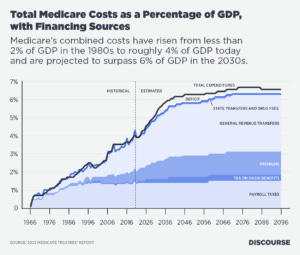

As Figure 2 shows, Medicare’s combined costs have risen from less than 2% of GDP in the 1980s to roughly 4% of GDP today and are projected to surpass 6% of GDP in the 2030s. This is an unsustainable rate of growth for a federal program. Medicare is consequently the leading driver of a federal fiscal situation that is rapidly spiraling out of control. Provisions of law that automatically increase spending on Medicare and other large mandatory spending programs are causing total federal spending to grow far faster than taxpayers can finance, as illustrated in Figure 3.

As Figure 3 shows, annual deficits (the gap between the two lines) are steadily increasing despite tax collections keeping pace with GDP growth. This is because federal spending is rising faster than U.S. economic output. This worsening federal fiscal imbalance, driven largely by Medicare growth, threatens Americans’ future economic security. The situation is worsening despite the fact that the federal government is persistently spending relatively less on everything else in the budget than Medicare, Medicaid, so-called Obamacare, Social Security and interest payments, as seen in Figure 4.

Figure 4 indicates that there was a surge in other federal spending in 2020-2021, in response to the COVID-19 pandemic. But apart from that brief surge, other parts of the budget have shrunk in relative terms even as there has been persistent growth in Medicare spending and in federal deficits.

Papering Over the Problem

Neither Medicare’s own finances nor the federal government’s overall fiscal position can be stabilized without legislative action to slow Medicare’s cost growth. This will almost certainly require both presidential leadership and bipartisan cooperation. But President Biden’s Medicare proposals would further damage federal finances while creating an illusory improvement in Medicare solvency. The president’s outline proposes to “credit” to the HI trust fund savings assumed from negotiating lower prescription drug payments. This is an accounting gimmick that would allow HI to spend more money than it collects from participants. The Biden administration proposes to build upon negotiating powers created in the Inflation Reduction Act. Those authorities pertain to Medicare drug benefits funded through its SMI trust fund—importantly, not to HI. If expanding those authorities successfully lowers prescription drug costs, that would save the federal government money, but not in the Hospital Insurance program. (Granted, there are indeed some Medicare drug benefits—specifically, inpatient treatments—provided through HI. Notably, however, if those HI drug costs were also successfully reduced, there would be no need for an additional “credit” to the HI trust fund as the president proposes: HI’s finances would improve naturally as a result of lower outgoing payments.) Basically, the president is proposing to allow Medicare HI to spend more revenues than it collects, by giving it permission to spend the proceeds of savings his administration projects elsewhere. Specifically, Table S-6 of the budget projects that expanded drug price negotiating authority will produce $200 billion in savings through 2033, and the White House outline indicates that this same amount—$200 billion—will be transferred to HI. Again, it bears repeating that such “credits” to the HI trust fund would be an unnecessary budget maneuver if these were savings within HI that actually improved its solvency. There are multiple problems with such a gimmick. First and most obviously, granting HI more spending authority to the extent there are savings in prescription drug costs elsewhere would eliminate any fiscal benefit—whether to the larger Medicare program or the federal budget as a whole—of having lowered those costs. But more concerningly, the administration’s proposal is to simply give up on the idea of keeping Medicare HI solvent in any meaningful way. If Medicare HI is allowed to tap and spend savings from other accounts, there’s no reason to stop with just claiming the savings from prescription drug payments. Anywhere and everywhere the federal government says it is spending less on something than it previously planned to, Medicare HI can be given permission to spend that money, simply by crediting those savings to the HI trust fund. If Medicare HI is given this permission to spend purported savings from the SMI programs, the very idea of HI solvency essentially becomes meaningless. At that point, HI would no longer be required to be self-financing. Lawmakers may as well just do away with the entire concept of the HI trust fund—or for that matter, the HI payroll tax itself—if they’re going to allow HI to spend money the program didn’t generate. For lawmakers to be able to say, “We spent less on Other Program X than we previously planned to; ergo, Hospital Insurance solvency has been extended,” deals a fatal blow to the very idea of a solvent Hospital Insurance system. The same problem exists with the provision to credit the Medicare net investment income tax (NIIT) to the HI trust fund “as originally intended,” according to the outline. This tax is currently collected on the investment income of single taxpayers with more than $200,000 in annual income, and married couples with income above $250,000. The NIIT is separate from the taxes on employment earnings that have historically financed Medicare HI. It’s an income tax. It’s not collected through payroll tax withholding, nor does it fund Medicare under current law. The longer history of why the NIIT finances general government operations rather than Medicare HI is a somewhat torturous one, with different explanations circulated as to why things are the way they are. The more important fact is that the NIIT already exists and is already bringing revenue into federal coffers. Granted, the Biden administration proposes to increase these investment taxes by roughly $650 billion through 2033, but it also proposes to redirect the current NIIT to the Medicare HI trust fund. Such a transfer would clearly worsen, not improve, the state of federal finances: It would increase Medicare’s authority to spend money that the federal government is already collecting, without an offsetting reduction in any other spending. One needn’t be a budget expert to understand why that makes federal finances worse. The Joint Committee on Taxation has estimated that the federal government collected roughly $43 billion from the NIIT in 2022, suggesting that collections from the current tax could exceed $500 billion from 2024 to 2033. In other words, transferring these credits to the Medicare HI trust fund would increase the government’s spending authority by roughly half a trillion dollars before so much as an additional dime in additional revenues are collected. This would be a dramatic worsening of an already dire fiscal situation. The proposed transfers of credits of NIIT revenues and prescription drug savings to the HI trust fund are smoke and mirrors—they would have the effect of improving the apparent solvency of Medicare while undoing any reality behind what solvency means. If Medicare Hospital Insurance is only “solvent” to the extent it is given money from other programs to spend, then its solvency no longer means anything.

The Costs of Failing To Meaningfully Improve Medicare Solvency

As is evident from the graphs presented earlier in this article, Medicare must be reformed to moderate its explosive cost growth. President Biden’s proposals to transfer credits from other budget accounts to the HI trust fund are harmful because while they would achieve no meaningful financial improvement, the accounting change would make it appear as though they had. In addition, the president’s Medicare proposals also include a few other items, such as capping cost-sharing for generic drugs and behavioral health visits, that would actually add to Medicare’s costs rather than reducing them. The president’s proposed increase in the Medicare HI tax on incomes above $400,000, from 3.8% to 5%, would be a real tax increase that would legitimately (though only temporarily) extend HI solvency. However, it is dwarfed in magnitude both by the other gimmicks contained in the proposal, and by the amount of the Medicare financing problem that can only be permanently closed by moderating program cost growth. There is another very important point to grasp here, though it’s obscured by the complexities of federal budget scoring: specifically, why the administration’s Medicare proposals would worsen the federal fiscal situation relative to current law. But this important point will not be apparent in a standard Congressional Budget Office (CBO) score of the administration’s proposals. By law, Social Security and Medicare HI are only permitted to spend money on benefits to the extent there are resources in their trust funds. At the point their trust funds run out, payments cannot legally be made. Thus, under current law, according to the Medicare trustees’ projections, when the HI trust fund depletes in 2028, Medicare HI payments would be cut by 10%. The point is not that lawmakers would allow this to happen, for they almost certainly would not. The point is that it is the law, and any full understanding of proposed changes to current law must accurately compare them to current law. This reality means that the Biden budget proposals to transfer credits to the Medicare trust fund are proposals to increase spending above and beyond what current law permits. If lawmakers transfer $200 billion in bonds to the trust fund as the administration proposes, then the trust fund would remain solvent beyond 2028 and current law’s 10% benefit cut would not take place. The effect of the transfers is thus to increase Medicare’s spending authority—for at least 25 years, according to the administration. Why won’t this be evident in a CBO score of the president’s proposal? Because the CBO operates under scorekeeping rules established by Congress—rules that direct the CBO to ignore the reductions in Social Security and Medicare spending that would occur when their respective trust funds run out. Since the CBO is instructed to assume that higher, full-benefit payments would be made anyway, even without trust fund resources conferring the legal authority to do so, the president’s proposed extension of the program’s spending authority isn’t scored as the spending increase that it actually is. Lawmakers would perform a valuable public service by asking the Medicare actuary’s office to calculate the true budget effects of the president’s Medicare proposals, taking into account the increase in Medicare’s spending authority that would arise as a result of extending HI solvency beyond 2028. This calculation would be an enormous public service for several reasons, and not just because it would better illuminate the effects of the president’s Medicare proposals. All proposals to improve Medicare solvency should be evaluated by this standard, to prevent budgetary mischief in the form of extending solvency by way of accounting gimmicks. Extending solvency obligates real additional spending, and lawmakers should be required to fully finance any such new spending, so as not to make a dire federal fiscal situation still worse. The Biden budget proposal eschews a focus on the policy challenge of correcting Medicare finances in favor of an emphasis on rhetorical points such as raising taxes on high earners (defined as those earning more than $400,000). However, it is precisely because these tax increases can’t come close to getting the job done, that the budget must resort to shell games to disguise the problem of rising Medicare costs. The public interest would be advanced immeasurably if the administration were to shift its focus from political messaging to problem-solving.

The Destructive Dynamic of Partisanship

The irresponsibility of President Biden’s Medicare proposals especially matters because of the president’s outsized influence on national political dynamics. It is virtually impossible to enact lasting solutions to Medicare’s problems without the president’s active participation. Beyond this, the president’s positioning makes it far less likely that other leaders on either side of the political aisle will even step forward to offer effective solutions. However, while the president’s irresponsibility is particularly damaging, he is not the only one exhibiting it: Many influential Republicans as well as many reporters are being just as irresponsible. Medicare’s untenable cost growth is a public policy problem with which neither major political party would prefer to deal. Responsible elected officials who note the necessity of addressing the problem do so because it is an unavoidable reality, not because there are great political benefits to doing so. And neither party finds it politically advantageous to admit to voters that the growth of Medicare spending must be slowed, or that Medicare taxes must be raised. This is why House Republicans have hastened to assure voters that their budget will not cut Medicare, while President Biden promises the same thing. Neither party feels safe in candidly discussing Medicare’s problems without the other’s participation, which is why Medicare reform must be bipartisan. Despite these realities, much media reporting about Medicare suggests that the only reason to deal with its cost growth is because of Republicans’ supposed ideological opposition to the program. A typical example can be found in a recent article in The Hill, which absurdly said that “Republicans have long favored cutting or even eliminating Medicare, Medicaid and Social Security.” This is a repeat of partisan Democratic spin—and it is also incorrect, as the Republicans’ frantic defensive reactions to President Biden’s positioning clearly show. Beyond this, there are the historical facts that Republicans actually expanded Medicare in 2003, and they have only been willing on rare occasion to slow the rapid growth of Medicare and Social Security—and only in concert with Democrats. Responsible reporting should neither traffic in partisan spin, nor should it be incorrect, but unfortunately the obvious mischaracterizations in The Hill article are both—and they’re by no means an uncommon example. Lest my summary of the problems with the president’s Medicare framework be misinterpreted as the vantage point of one side of the aisle, I would note that several House Republicans are reportedly positioning themselves to be even more irresponsible. Determined to avoid charges that they would cut Medicare and Social Security, but equally determined to still be seen as favoring lower taxes and a balanced budget, these members are embracing a budget framework that would spend roughly 60% of the federal government’s non-interest budget by 2032 on just two programs—Social Security and Medicare—even under the proposed budget’s fantastically rosy assumptions. (Under more realistic assumptions, nearly two-thirds of the non-interest budget would go to those two programs alone.) Such positioning by House Republicans on the budget would be grossly irresponsible from several perspectives. Substantively, no nation with an interest in its future can afford to spend the preponderance of its federal resources solely on benefits for the aged. Politically, however, it would be especially nonsensical for Republicans to position themselves in this way. Republicans are increasingly the party of working-class wage-earners, yet this budget framework would position the party as favoring a vision in which the taxes paid by working families with children would return dramatically less in basic functions of government, only so that the vast majority of those taxes can be redirected toward benefits for elderly Americans with higher average incomes. For all the problems with President Biden’s Medicare proposals, they at least serve a coherent political position from the vantage point of his party’s base. The same cannot be said of the proposals under consideration by several House Republicans, which fail to add up either substantively or as a philosophical statement. Regardless of how other members of Congress position themselves, President Biden’s Medicare budget proposal is a counterproductive offering. It would improve the appearance of Medicare’s accounting while worsening its actual problems as well as the federal fiscal imbalance, by giving Medicare Hospital Insurance permission to spend money the program didn’t generate. As a political document, the White House’s Medicare framework sets the country back by making it less likely the parties can cooperate on much-needed reforms. It’s a shell game, with American voters as the mark.