The Inflation Surge Is Coming to an End

By David Beckworth and Patrick Horan

Americans continue to feel the pain from higher prices. Over the past year, consumer prices have risen rapidly and recently reached a level not seen since the early 1980s. This surge in inflation has crushed consumer confidence and become a hot political topic that could have a bearing on next year’s elections. Moreover, the current inflation rate has some observers worried that inflation fears could spiral and pull the U.S. back into a 1970s-like inflation quagmire.

So should we be worried? In October, we argued that the answer was no. We still hold this view but now see the inflation surge persisting into the first part of 2022. Afterward, inflation is likely to start falling toward its 2% target. Here we explain why this outcome is likely and, along the way, show how a mix of stable aggregate demand growth and healthy capitalism can provide much good for society.

It’s Not the Level of Demand, But Its Composition

At the end of the third quarter of 2021, total dollar spending on the economy was back to where it would have been had there been no pandemic. This robust recovery in total dollar spending, or nominal gross domestic product (NGDP), was due to the large injections of cash from Congress and the accommodative monetary policy of the Federal Reserve. Some observers view this support as creating excessive demand for goods and services, contributing to shortages and spawning the recent surge in inflation.

But had there been no pandemic, the economy would have reached its current size at a normal pace with the same low inflation rate that prevailed before the pandemic, as shown in the figure below. The level of demand, therefore, cannot be the main culprit for the inflation surge through the third quarter of 2021.

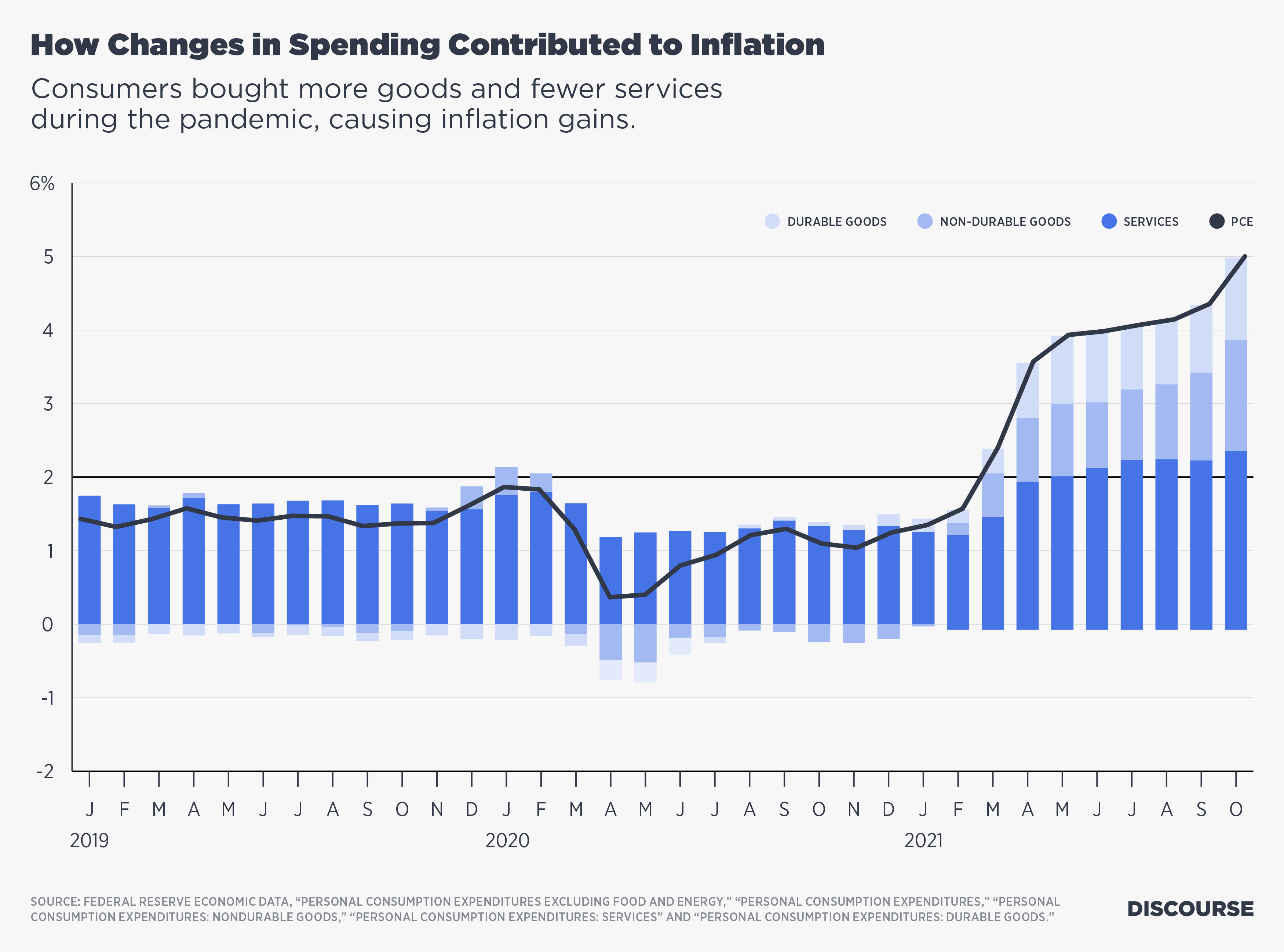

A better explanation for the higher inflation through this period is the change in the composition of total dollar spending. During the pandemic, households shifted away from spending on services—eating out, travel, leisure, etc.—because of COVID concerns and increased their expenditures on physical goods they could use at home, where they were stuck. As a result, spending on services declined below pre-pandemic levels while spending on goods rose above pre-pandemic levels. This shift in consumer spending preferences was imposed on an economy that was not equipped for it and was still in the process of reopening. As a result, this change in the composition of aggregate demand created supply chain bottlenecks, production problems and inflation.

This explanation is illustrated in the figure below. It shows the inflation rate (black line) for Price Consumer Expenditures (PCE) and the impact on inflation from services (dark blue bars), non-durable goods (medium blue bars) and durable goods (light blue bars). Durable goods are those that do not wear out quickly, such as cars and appliances, while non-durable goods such as food and clothing do. Before the pandemic, durable goods consistently added modest deflationary pressures while non-durable goods were on balance neutral.

Spending on services, however, was persistently inflationary and was in fact the main driver of PCE inflation. But starting in the spring of 2021, the goods components became increasingly important as their share of consumption spending rose and prices soared. Inflation due to services spending rose as well, but the lion’s share of the inflation gains is coming from goods consumption.

It is worth noting that in Asia, where the pandemic proved less destabilizing, the shift in consumption from services to goods was far milder. As a result, Asia did not have the surge in inflation seen in the United States and Europe, even though some countries such as Japan, Thailand and Vietnam ran large budget deficits. The composition of demand, then, is key to understanding most of the U.S. inflation surge of 2021.

Time and Capitalism Will (Mostly) Heal the Inflationary Wound

The good news is that the shift in consumption spending is likely to reverse itself and undo much of the recent inflationary pressure. All that is needed is time and the power of capitalism.

Time will help on two fronts. First, as the pandemic ends and the federal fiscal support fades, household demand for daycare, travel, dining and other services should grow and demand for goods decline owing to budget constraints. Second, durable goods consumption cannot stay elevated for long since there are only so many desks, computers, exercise machines, etc. that a household can use. Over time, this physical constraint will become binding too.

In addition to time rebalancing the composition of demand, capitalism should also help reduce goods inflation. To see why, first note that the surge in goods prices, and therefore PCE inflation, is largely tied to the soaring price of commodities over the past year. Despite the real pain of these higher prices, there is a silver lining to them: They create expectations of higher future prices and, therefore, expectations of higher future profit margins from increased production. At the same time, higher prices lead consumers to look for cheaper substitutes. Between these two forces, prices will begin to fall. This is why we are already seeing ocean freight rates and oil prices declining, while automakers are finding various work-arounds to computer chip shortages.

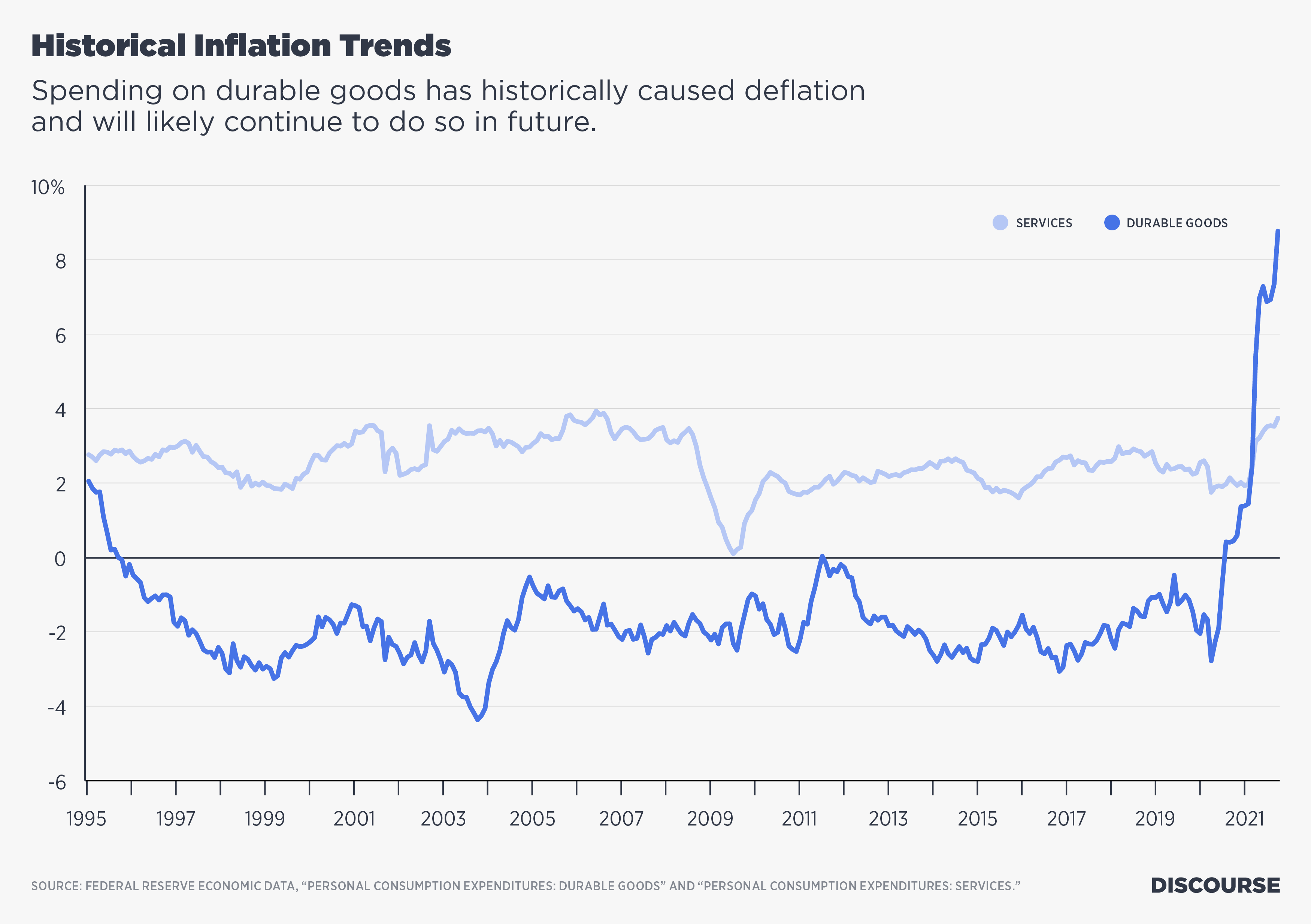

To be clear, to fully unleash the power of capitalism we need to get to the other side of the pandemic. But once we do, we can expect goods prices to decline significantly. To illustrate the potential for this deflation, the figure below shows the historical trends for services and durable goods inflation in the decades leading up to the pandemic. As noted earlier, services inflation has always been positive. Durable goods, on the other hand, averaged 2.2% deflation over the same period.

This amazing 25-year deflationary trend is a testament to the power of global capitalism finding ways to cut production costs. Even President Donald Trump’s trade war was not enough to end this long deflationary run. These same global market forces are likely to significantly lower the cost of goods as the pandemic ends. Put differently, the 10-plus percentage point jump in the goods inflation rate over the past year simply is not sustainable in the face of these powerful market forces. Likewise, the inflationary pressures on non-durable goods prices should also ease for the same reason.

U.S. Monetary Policy Is Still Credible

The optimistic view that time and capitalism will eventually end most of the inflation surge assumes that growth in aggregate demand will remain relatively stable. We believe this is a reasonable assumption for several reasons.

First, the large pandemic spending packages are coming to an end. Future fiscal policy, while still generating deficits, will be far more manageable and modest in size, as seen in the low interest rates on long-term Treasury securities. One interpretation of these low Treasury yields is that the bond market anticipates strong demand for government bonds because people and firms, both domestically and internationally, will prefer to hold onto bonds as a form of liquidity rather than spending on goods and services. So the low Treasury yields indicate that inflationary pressures will be kept in check.

Second, the Fed is already signaling a tightening of monetary policy through its public statements on future interest rate hikes and on its desire to more rapidly taper its asset purchases. It will follow up with actual interest rate hikes over the next year. We believe this is appropriate and that the Fed will accelerate tightening if needed to tamp down inflation fears.

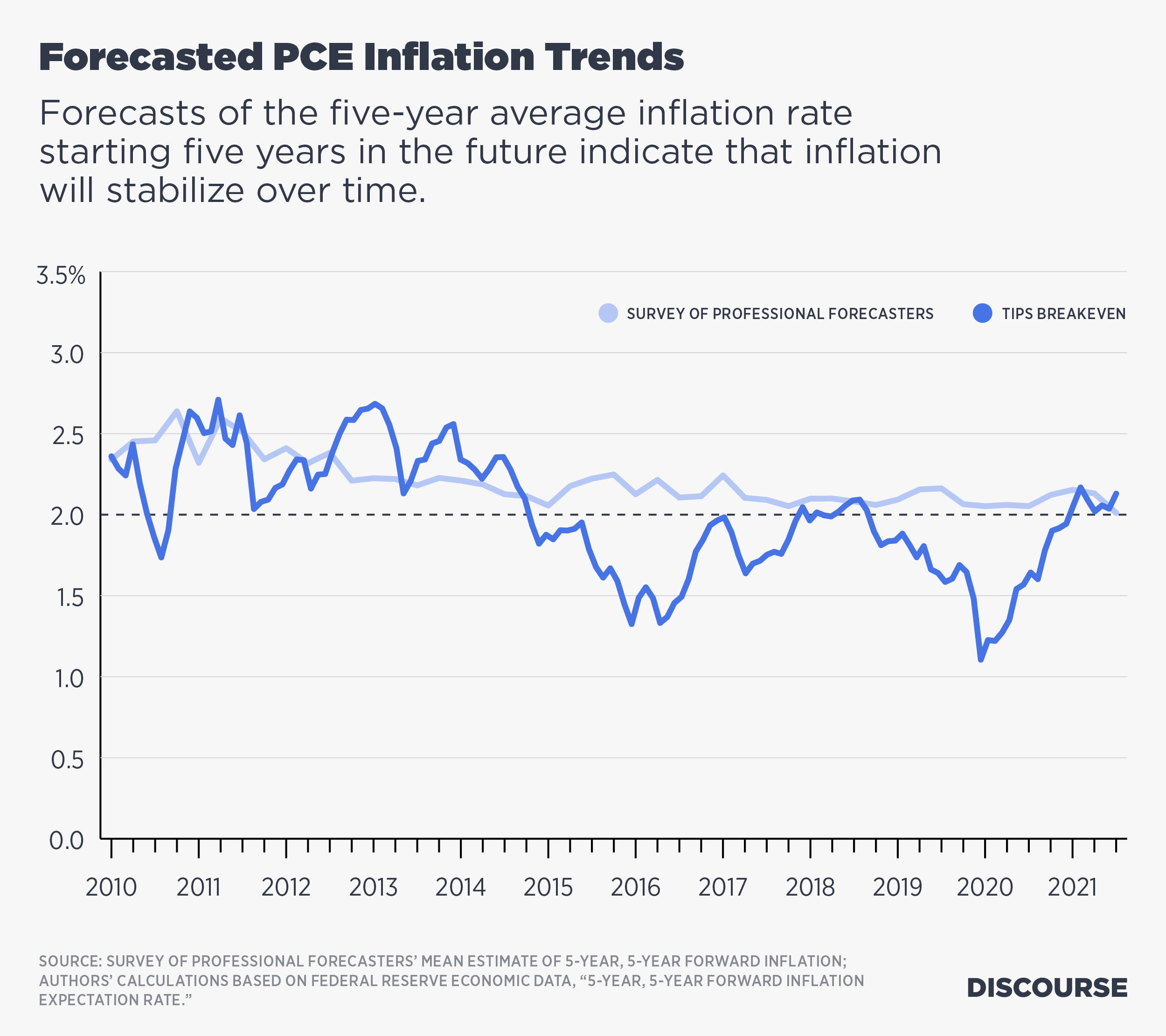

Forecasters believe that the Fed will keep inflation in check, leading to steady and stable growth in demand over the long run. The figure below shows two measures of the forecasted increase in the PCE over a five-year period, five years into the future. The first measure comes from the Survey of Professional Forecasters, while the second is the implied rate from the Treasury market that is called the “TIPS Breakeven.” This second rate is determined by market participants with “skin in the game.” Both forecasts look beyond the near term where pandemic-related disruptions affect inflation. Inflation trends this far out should largely reflect future monetary policy and therefore reveal whether forecasters think the Fed can maintain long-term price stability. Both forecasters and markets see no sustained increase in the trend inflation rate at this horizon. Fed policy for them is still very credible.

No Time for Complacency

The inflation surge of 2021 caught many by surprise, including us. It has caused real pain for many people, it could affect 2022 election outcomes, and it has some worried about a return of 1970s inflation levels. Nonetheless, it is important to understand that at its core, the 2021 inflation is a product of the pandemic more than anything else. Consequently, policymakers should aim to see through inflation caused by pandemic disruptions while also making sure that monetary policy tightens sufficiently to keep the growth in aggregate demand stable.

Some concerned observers point to the latest forecasts for nominal GDP growth, which put it above its pre-pandemic trend. These deviations, however, are modest and forecasted to be temporary. Moreover, they are nowhere near large enough to generate an inflationary spiral like the one seen in the 1970s.

The figure below illustrates this point by comparing NGDP deviations from trend going into the Great Inflation with the NGDP deviations from trend going into the next decade. NGDP at its peak is forecasted to be about 2% above its pre-pandemic trend and will gravitate back to it. On a comparable timescale, the 1970s deviation from trend reached a peak of 36%. From this perspective, then, there is no need to worry about another Great Inflation.

The Fed’s recent tightening of monetary policy indicates it does not take this forecasted stability for granted and will do what is necessary to keep NGDP growth stable. Between this effort and the healing ability of time and capitalism, we feel confident that the recent inflation surge will begin to fade in 2022. The slowing of inflation will confirm the confidence markets have in the Fed.