Market Discipline First Requires Policy Discipline

To combat the negative effects of previous misguided fiscal and monetary policies, U.S. policymakers should cultivate national self-discipline and focus on long-term growth

By Thomas Hoenig

The U.S. economy is the envy of the world. The United States’ commitment to the rule of law, its entrepreneurial culture and its deep and vibrant capital markets have enabled it to build enormous wealth. Its per capita GDP ranks among that of the top 20 wealthiest nations. This success also has rested on America’s adherence to disciplined fiscal and monetary policies, which over time have provided for low inflation and a sound, stable currency trusted throughout the world. However, in recent decades the U.S. approach toward the economy has changed. Fiscal and monetary policies have become tools to manage the economy and extend short-run bursts of economic activity, ignoring their too often negative long-run consequences.

The U.S. is now experiencing some of these negative effects, including a significant increase in its national debt, increased volatility within financial markets, high inflation and a decline in real GDP growth. To combat these problems, U.S. policymakers should recalibrate fiscal and monetary policy to focus on long-term growth.

Expanding the Role of Fiscal and Monetary Policy

In reaction to the economic and financial crises that have occurred over the past two decades, the U.S. government repeatedly initiated spending programs of unprecedented magnitudes. While stanching the immediate crisis, these programs were extended well past the crisis and into the economic expansion that followed. The government’s response to the recent pandemic is illustrative: The Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed in March 2020, provided for roughly $2.2 trillion in new spending over the next decade, which increased federal spending from $4.4 trillion to more than $6.6 trillion—a 50% increase—between 2019 and 2020 alone.

As intended, the economy immediately began to recover. However, the increased spending continued into 2021 and 2022. In December 2020 the Consolidated Appropriations Act was passed, followed in March 2021 by the American Rescue Plan Act, which increased spending by $2.3 trillion and $1.9 trillion, respectively. These actions, moreover, followed a pattern similar to that taken during and following the financial crisis of 2008, so that by 2019, well before the pandemic, annual federal government spending had increased from $3.1 trillion to $4.5 trillion.

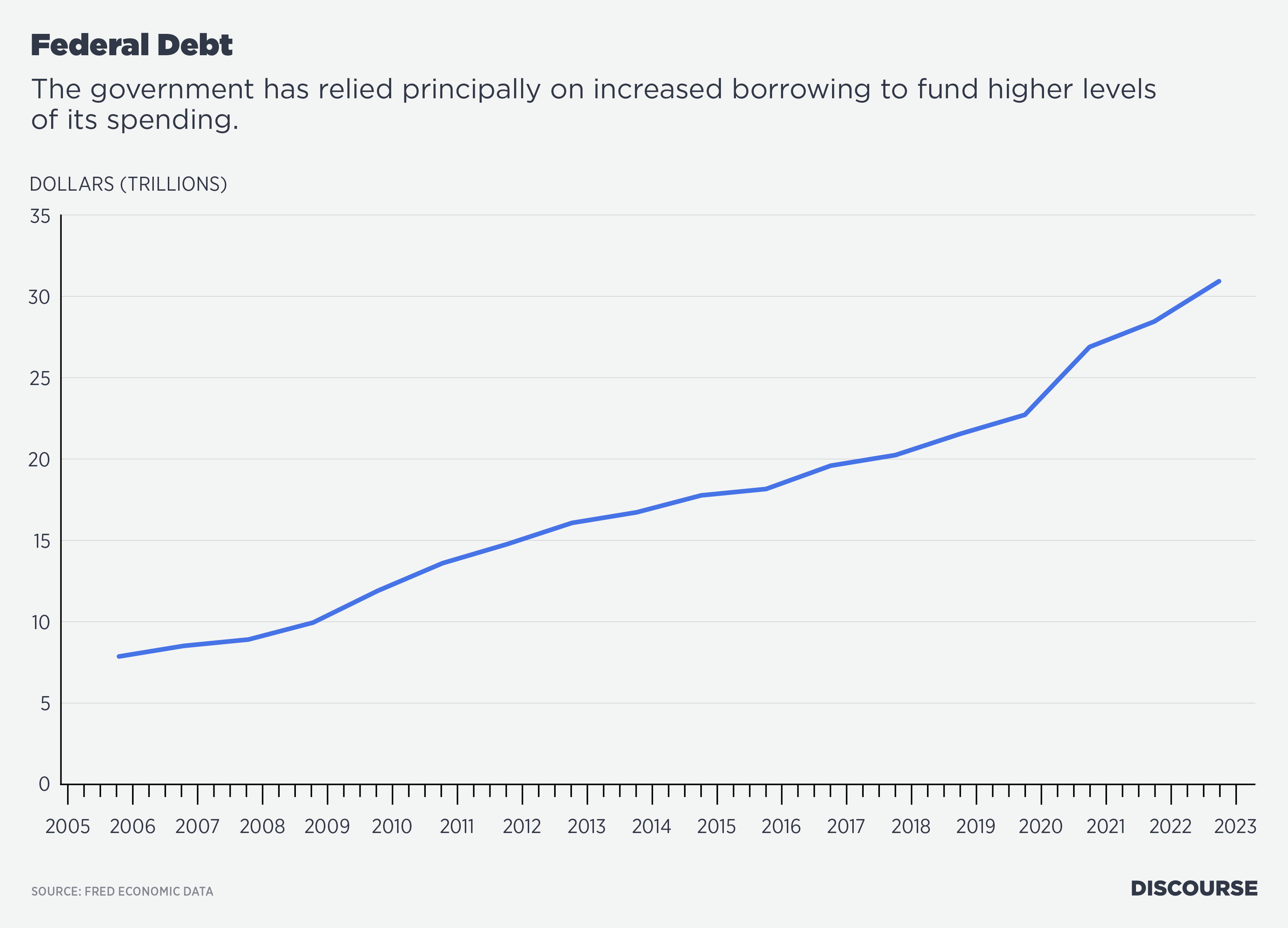

Significantly, the source of this spending was not from tax revenues but from increased government borrowing. Between 2019 and 2021 alone, outstanding U.S. gross debt increased from $22.7 trillion to $28.3 trillion, and today it stands at $31.5 trillion. By comparison, federal gross debt was a mere $9.0 trillion as recently as 2007.

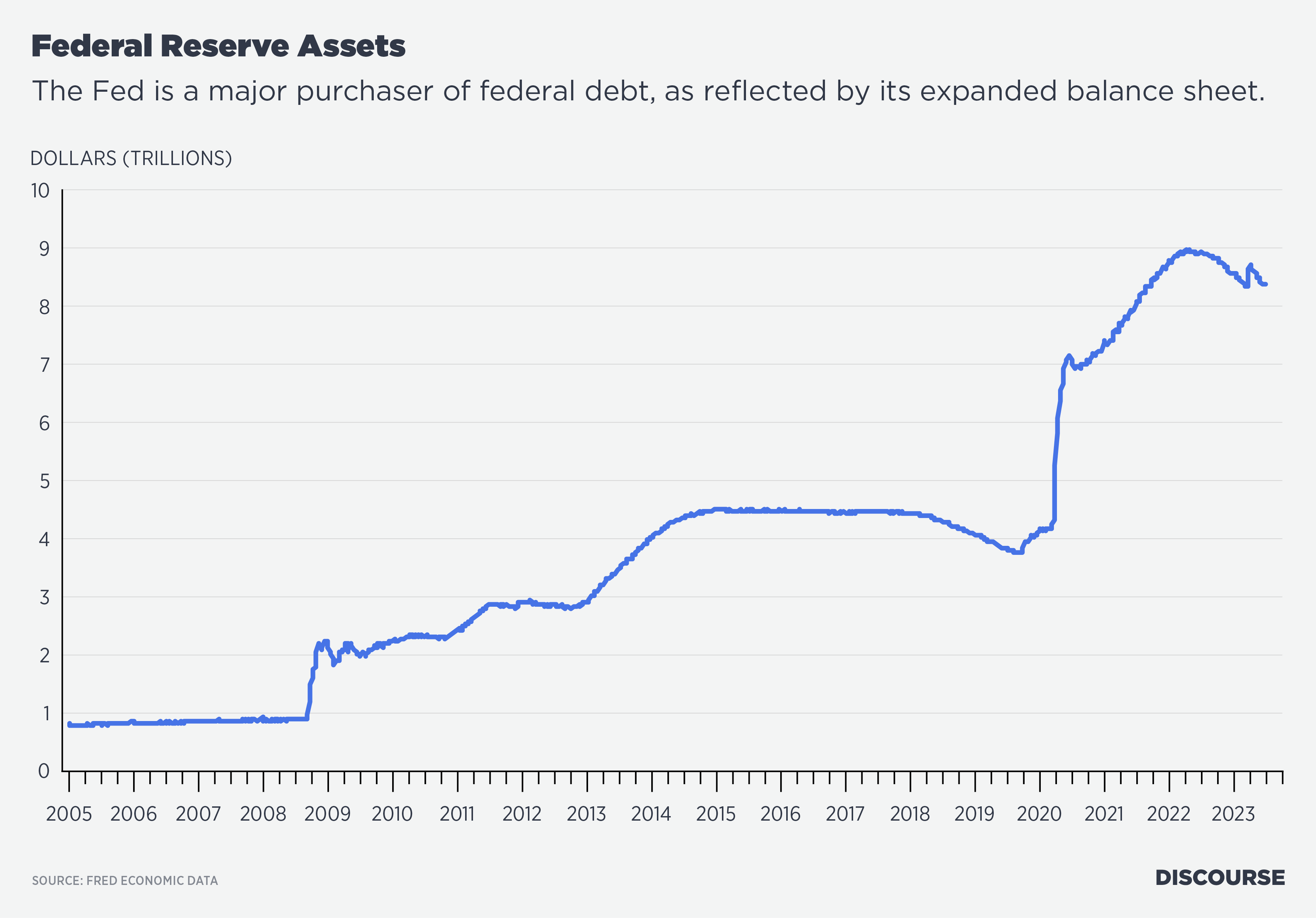

The sources funding this massive debt include not only domestic and foreign lenders, but a third source of ever greater importance, the Federal Reserve System (Fed). In 2010 the Fed began a massive operation to increase its purchases of government and government-guaranteed debt, a process known as quantitative easing. From then to the present, the Fed has increased its balance sheet from $2.2 trillion to nearly $9 trillion at its peak while suppressing interest rates to near zero. Between 2020 and 2022 alone, the Fed increased its holdings of Treasury debt by $3.6 trillion, paying for this expansion with freshly created liabilities.

It shouldn’t be surprising that following these actions, the U.S. has consistently experienced inflation. Initially this took the form of asset inflation, as the median price of a home, for example, more than doubled and average equity prices tripled between 2010 and 2022. Inflation of goods and services took longer to germinate, but in June of 2022 it reached a 40-year high of 9%. Today, core inflation remains near 5%, 3 percentage points above the Fed’s target.

Coincidently, as inflation has increased, U.S. productivity and real incomes for working Americans have declined. U.S. productivity has fallen from 2.3% during the 1990s to less than 1.4% during 2008-2018, and it remains subdued to this day. And although nominal wages are rising, real wages have fallen as productivity has declined and inflation has exceeded nominal wage gains. For all their good intentions, neither the federal government nor the Fed has delivered stable prices, sustained increases in economic productivity or real wage gains, all of which are necessary for increasing the wealth of a nation.

Confronting the Future

If the U.S. intends to preserve its economic success and power, the federal government cannot continue to spend money nor the Fed continue to buy up U.S. debt without limit. However, there is little evidence that either the government or the Fed is committed to changing the policy model, as recent Congressional Budget Office (CBO) projections show.

Earlier this year, the CBO released its fiscal projections for the next decade, which are striking in their implications. For example, the federal debt held by the public will increase $22 trillion by 2033, to a level of $46 trillion, or 118% of GDP. The federal deficit will exceed $1.4 trillion in the current fiscal year and is projected to reach nearly $3 trillion by 2033, or 7.3% of GDP. Interest on the debt alone will exceed 3.5% of GDP by then.

Having a nation’s debt grow faster than its income is not sustainable. It places upward pressure on interest rates, slows private investment and constrains real economic growth. Among the CBO’s projections, for example, real GDP falls from an average longer-term historical rate of 2.3% per year to 1.8% for the decade ahead. Such a slowdown could cause the nation’s real income to be as much as $1.2 trillion less than what it would have been at the higher growth rate.

These data and projections show the U.S. is on an unsustainable path in which its national debt accelerates over the next decade and its economy becomes less dynamic. Should this occur, the political pressure to monetize the emerging debt by printing even more money will become severe and persistent.

Making Hard Choices

Given these projections, it appears that U.S. leadership must ultimately choose among three options in managing the growing federal debt and inflation outlook. Each choice has its own set of consequences, and each involves different long- and short-term tradeoffs. How well leadership chooses will define how well the future economy performs and how wealthy the U.S. remains.

Option 1: Debt Monetization

The first option is for the government to continue spending beyond its revenue and for the Fed to accommodate this spending by monetizing the rising federal debt. The Fed becomes the Treasury’s printing press. Under this option, the Fed’s balance sheet continues to expand, bank reserves grow and interest rates are artificially suppressed. The policy initially may appear beneficial for the economy. But as we are learning now, if it goes unchecked, the outcome is almost always higher asset and other price inflation and ultimately a loss of confidence in the value of the currency and the economy. Walter Bagehot’s famous dictum about banks holds equally true for governments—once their soundness is questioned, it is too late. At that moment, governments and their citizens are forced to make sizable, painful fiscal adjustments.

We have seen this play out repeatedly in history around the globe. Turkey and Argentina are recent examples of countries where political pressure and an acquiescent central bank led to significant debt monetization and inflation. This has been the path of the U.S. in recent years, and the results are becoming increasingly apparent, difficult to manage and unpleasant. Ultimately, this path also generates more social unrest and conflict. The risk for such an outcome has increased for the U.S.

Option 2: A Temporary Stalemate

The second option, while better for the economy in the longer run, is hardly optimal. It involves a stalemate between the fiscal and monetary authorities. In this instance, the fiscal imbalance grows while an independent central bank maintains its focus on long-run price stability and resists the fiscal authority’s call to monetize its debt. Under these conditions, a negative fiscal outlook inevitably undermines the government’s ability to borrow at low rates. As deficits grow at a rate faster than national income, the market demands a higher debt risk premium, accelerating fiscal strife.

This option is the one currently in place as the federal debt is projected to accelerate going forward and the Fed aims to end its purchase of federal government debt. If the Fed keeps its commitment to hold relatively less public debt, the government will increasingly compete with the private sector for funds, and it will drive up not only the government’s borrowing costs, but also the real cost of borrowing for the private sector. Eventually, this combination of large debt and higher cost of capital weakens economic growth and undermines confidence in the economy’s long-run growth potential. It ends in economic crisis and either the capitulation of the central bank (and a return to Option 1) or real reform.

Option 3: Reform

The most responsible option for resolving the increasingly difficult U.S. fiscal and monetary policy challenges is to agree that the nation’s debt cannot grow faster than its income indefinitely, and to restore discipline to both policies. It requires that the Fed not only be independent but act so. If the Fed holds to a disciplined money policy, the government must accept that the Fed will not monetize excessive deficits. Instead, the government will have to develop a credible long-term plan to reestablish fiscal balance.

Such a plan must be clear, have the force of law and have measurable indicators of progress. Under these conditions, the U.S. has a much greater chance of reassuring markets and the public that the country can service its debts with a reliable, stable currency. While the transition will involve significant spending and revenue adjustments and a temporary slowdown in economic activity, it will restore the nation’s saving and investment balance and provide for more stable interest rates. It also will be more aligned with the goal of providing stable, long-term growth.

One additional point: To be broadly accepted, the plan must be seen as fair and have a sense of shared sacrifice across all segments of the economy. This is particularly important as regards entitlements and subsidies to special interests. Entitlements comprise nearly two-thirds of U.S. spending today and, as made clear in the recent CBO projections, must be reduced to assure that U.S. debt grows more slowly than its national income, thus reducing its debt-to-GDP ratio to a more sustainable level.

In this regard, Congress must disappoint a host of special interests, as the cost of subsidies significantly reduces the government’s revenue stream. This reform means controlling budget earmarks, trimming subsidies to numerous economic sectors, and resolving our banking problems and the perception that, for example, Wall Street is favored over Main Street. Without this commitment to an evenhanded policy, such an effort will only foster mistrust and cynicism among the public. Leaving these issues unaddressed will undermine the essential support required for the tough decisions needed to bring the federal budget toward balance.

An example of how this could develop for the U.S. is hinted at in Canada’s not too distant past. At the start of the 1990s, Canadian federal debt had increased to 73% of GDP and was still rising, with the deficit running at 6% of GDP. At the same time, the Bank of Canada targeted a steady downward path for inflation from 3% toward 2% by the end of 1995. With no monetary accommodation from the central bank, persistent government deficits caused real interest rates in Canada to climb. While Canadian inflation was below that of the U.S., its borrowers paid a premium over U.S. rates. Moreover, because of Canada’s sizable deficits, its dollar came under persistent pressure. Overall economic performance suffered, with GDP growing sluggishly and unemployment reaching as high as 12%.

These economic conditions caused the government to change course and make a credible commitment to balance the budget. In the following years, the federal budget deficit fell dramatically. Revenue increased and government expenditures were cut sharply. By 1996, Canadian interest rates had fallen below comparable U.S. rates. Inflation remained subdued, real GDP growth picked up and unemployment fell. The result was a stronger economy and a useful illustration of what can be accomplished with the right policy.

Cultivating National Self-Discipline

There are no shortcuts. The U.S. must adjust from poorly disciplined national fiscal and monetary policies to ones that look to the nation’s long-run future. There is no way to avoid pain in fixing the fundamentals of the economy. Such discipline can be inconvenient for the election cycle, and it is undeniably harsh to some if the economy enters a recession and unemployment rises. But shortcuts now mean more people out of work later because the federal government is unwilling to make hard choices. Outlining a credible course for managing the national debt will accelerate the restoration of confidence in the U.S. economy and contribute importantly to sustainable capital investment, job growth and increasing national income and wealth.

The fiscal projections for the U.S. are so stunning that reform must occur. The U.S. government must discipline itself and adjust its spending and tax programs. The monetary authorities must cease enabling the government’s excess spending. It is that simple and that difficult. If preemptive corrective action is not taken in monetary and fiscal policy, then the U.S. risks precipitating its own next financial and economic crisis.