Biden’s Strategy To Fight Inflation Ignores Its Root Causes

The administration should focus on fixing monetary and fiscal policy, not increasing government spending

By Veronique de Rugy and Jack Salmon

Writing in The Wall Street Journal, President Biden explains his plan for fighting inflation: housing subsidies, clean energy tax credits, more government spending (which he calls “investments”), more Medicare spending, price control regulation for foreign ocean freight companies and more. The president also wants to cut the deficit without implementing any reductions in spending. In addition, the president has full faith in the anti-inflation actions taken by Jerome Powell, the chair of the Federal Reserve.

We are very skeptical that this plan will work.

The Inflation Problem

The U.S. has an inflation problem, and it will continue to have an inflation problem—meaning inflation above the Fed’s 2% target—for a long time. We arrived here through over-stimulative monetary and fiscal policies, the Fed’s incomprehensible slowness to acknowledge an inflationary problem during most of 2021 and the Fed’s failure to act to reverse the trend to this day. All that is compounded by the latest unexpected supply shock due to the Russian invasion of Ukraine.

The U.S. Department of the Treasury first issued $2.7 trillion of new debt, which the Fed quickly bought in exchange for $2.7 trillion of new reserves that the Treasury then sent out as checks and other forms of stimulus and COVID-relief payments to Americans. The Treasury then borrowed another $2 trillion or so to send out another round of checks and payments. Overall, from the last quarter of 2019 to the second quarter of 2020, federal debt rose by almost 30% of GDP. Some debt has since been inflated away, but it still remains about 20% higher than pre-pandemic levels.

The purpose of this massive response was meant to give people money to stimulate the economy and fill the so-called output gap. But this approach was problematic to start with because it was meant to correct deficiencies in aggregate demand, not supply-side problems caused by the pandemic and government lockdowns. However, the $5 trillion injected into the economy was larger than any plausible output gap at the start of the pandemic.

It made even less sense to adopt the $1.9 trillion American Rescue Plan in March 2021. Around early 2021, the Congressional Budget Office projected that the output gap would be $700 billion through 2023, the period when most of the statute’s appropriations would be spent. In other words, $1.9 trillion was double to triple what was needed to fill the gap. Meanwhile, the economy was growing, and unemployment was already way down from a peak of more than 14% to 6 percent in March of 2021.

Massive spending boosted aggregate demand without an equal increase of the supply capacity of the economy: Inflation was inevitable.

Faulty Explanations

However, you wouldn’t know the cause of inflation by reading the president’s op-ed. Here is his only mention of some causes for inflation: “Inflation is elevated, exacerbated by Vladimir Putin’s war in Ukraine. Energy markets are in turmoil. Supply chains that haven’t fully healed are causing shortages and price hikes.”

No mention of spending. In fact, spending was encouraged and cheered. For instance, look at what Chairman Powell said in February 2021 about the ARP:

In the near term, policies that bring the pandemic to an end as soon as possible are paramount. In addition, workers and households who struggle to find their place in the post-pandemic economy are likely to need continued support. The same is true for many small businesses that are likely to prosper again once the pandemic is behind us.

As inflation became harder to ignore, Powell continued to focus on labor-market indicators and stories about supply constraints while ignoring aggregate demand. This is what he said in June 2021:

Congress and the Biden-Harris administration have accelerated the recovery. . . . The American Rescue Plan also delivered desperately needed financial assistance, which has been and will continue to be a lifeline for American families. The American Rescue Plan provided direct relief checks, extended unemployment, and increased healthcare access. And we have seen the results of that extraordinary action. Over the last four months, the economy has added over 1.6 million jobs, and new unemployment insurance claims have dropped significantly.

To be fair to Powell, many economists seemed oblivious to the impact of monetary and fiscal policies on aggregate demand, cheering ARP spending and dismissing fears of overheating. Instead, they joined the chairman in blaming pandemic-induced supply-side restraints, including semiconductor shortages, workers’ reluctance to rejoin the workforce and new COVID variants.

This mistake was stunning, considering that in the course of 2021 real economic growth was strong (U.S. real GDP grew by 5.5%, and nominal GDP grew by around 11.5%), throwing cold water on the supply constraint argument. Indeed, it’s hard to argue that supply constraints were too small to prevent strong real economic growth yet big enough to be the main cause of inflation.

Additionally, if global supply chain constraints were the problem, how can we explain the large difference in inflation between countries in Europe and the U.S.? After all, global supply chains affect everyone. It makes more sense to explain that difference by comparing the size of COVID relief spending in the U.S. with that of European countries before the start of the war in Ukraine.

You could get whiplash from listening to economists and the Fed chairman call for COVID relief to stimulate aggregate demand, but then shift to argue that inflation was entirely supply driven. Yet such was the state of the world then, and things haven’t change much today. The reappointments of Lael Brainard as Fed vice chair and Powell as leader of the Fed suggest that they will not be held accountable by Congress for the current inflation. Likewise, legislators fail to grasp how their COVID largesse pushed up prices, as they are constantly angling to spend even more.

Examining the Evidence

The president’s op-ed shows that no one is yet willing to take ownership of this catastrophic failure. The Federal Reserve has adopted a more hawkish message when it comes to inflation, but it continues to issue projections of inflation falling back to trend, persisting in this oblivious optimism although Fed policies are still accommodative for the current inflationary environment. The central bank’s purportedly anti-inflation monetary policy will leave real interest rates in negative territory even after several rate hikes. In other words, the Fed’s message for well over a year now has been that inflation will fall on its own after supply disruptions are resolved. But its predictions have been consistently wrong, and it has revised its forecast upward at every meeting, as the chart below shows.

Supply constraints are real and have contributed to the rise in the price level. But there can be little doubt that America’s inflation problem, which started long before the Ukraine invasion, is mostly the result not of supply problems, but of the creation of excessive purchasing power.

Many other studies make the same points. Back-of-the-envelope estimates by Federal Reserve economists find that fiscal stimulus contributed about 2.5 percentage points to U.S. inflation in the last quarter of 2021. This represents about half the excess inflation above the 2015-19 baseline. Similarly, an IMF study finds that about half (55%) the increase in producer prices (PPI) in 2020-21 is the result of demand, not supply factors. These producer prices are ultimately reflected in consumer prices due to increasing costs of production.

Recent research by the Federal Reserve Bank of San Francisco finds that about 3 percentage points of the increase in Core CPI in the last quarter of 2021 were driven by fiscal stimulus. Absent fiscal stimulus, Core CPI at the end of 2021 would have been around 2%, not 5%, as shown in the figure below.

The Role of Supply Shocks

There is no doubt that we now face a large supply shock because of the war in Ukraine. This shock is boosting the price level through higher oil and gas prices. (Here is one explanation of the difference between inflation and supply-shock boosts of the price level.) But inflation was on its way long before the war started.

What about other supply shocks? Here are some of the most common arguments we’ve heard and continue to hear about the ongoing inflation surge as the consequence of supply-chain issues, without properly acknowledging demand factors.

Argument #1: Inflation is due to supply chains being cut off or damaged.

The supply-chain issue was confronted during the first few months of the global pandemic, but supply chains have since proven to be remarkably resilient. The ports of Los Angeles, Long Beach and New York/New Jersey are responsible for about half of container shipping trade volumes in the U.S. As the figures below reveal, monthly data on loaded import volumes since January 2020 show that none of these ports seem to be underperforming compared with pre-pandemic norms.

Most of the remaining supply problems are rooted in elevated levels of demand.

Argument #2: Nominal spending has only barely returned to pre-pandemic trends in the U.S.

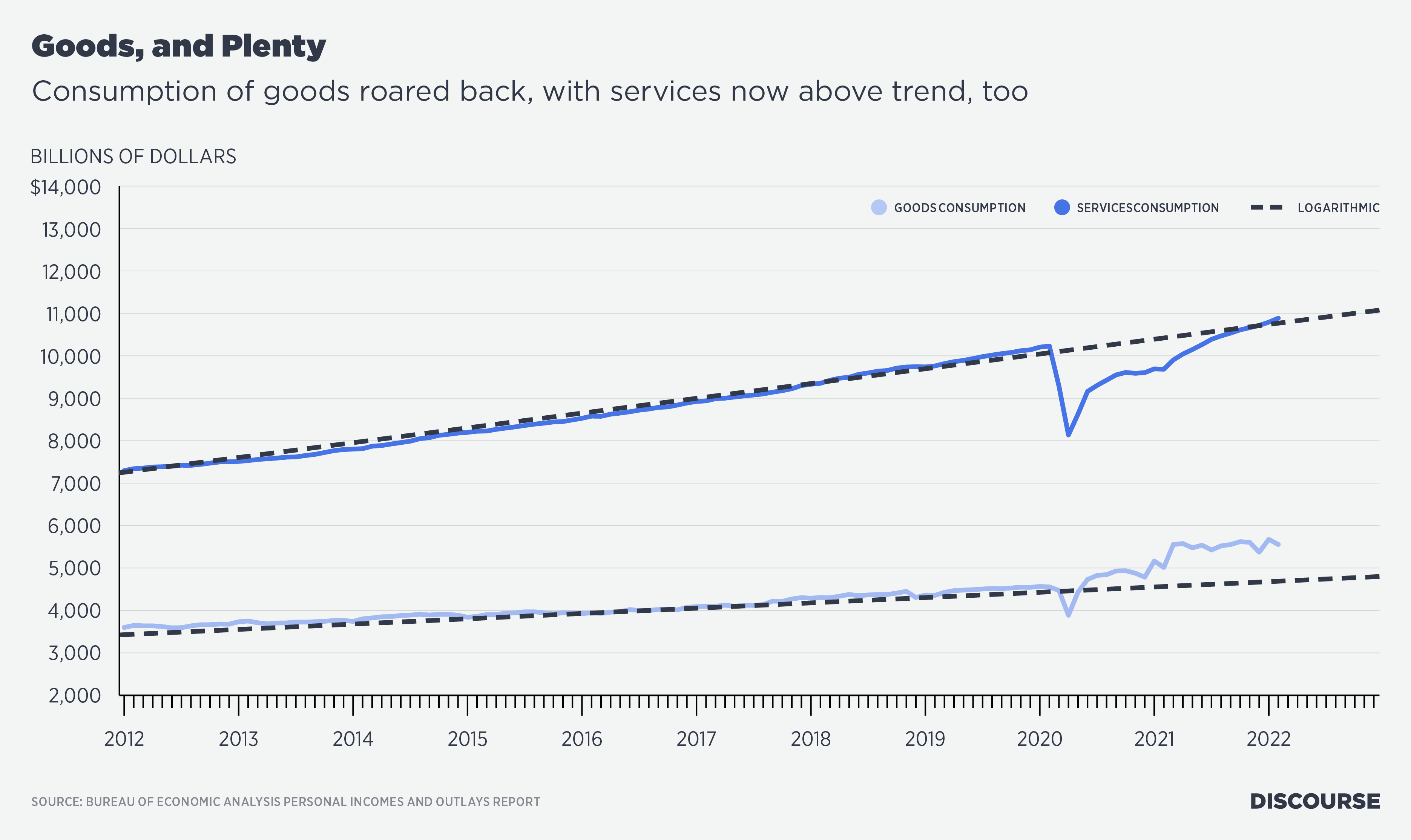

The notion that consumer spending has barely returned to pre-pandemic levels overlooks the preponderance of economic data. As the below figure shows, service consumption is back on its pre-pandemic trend, while goods consumption remains significantly above trend—although some economists continue to suggest that, by contrast, service spending “remains correspondingly depressed.”

It is important to note, however, that shortages do exist for some particular goods. For example, retail inventories remain below pre-pandemic trends, although these shortages are concentrated among some very specific items—namely, cars and car parts. Further, excluding vehicles and vehicle parts from the inventories, retail supplies are well above trend levels, as the below graphs indicate.

Not only do supply-side excuses completely overlook the data on restored supply chains, they also ignore the massive elephant in the room—namely, fiscal inflation and demand factors.

Core inflation shows that most of the inflation experienced in the Euro Area is indeed supply related. However, the chart below demonstrates that a large gap opened between Euro Area and U.S. core inflation in the spring of 2021. This gap remains very large, suggesting that U.S. inflation dynamics are less dependent on supply-related issues.

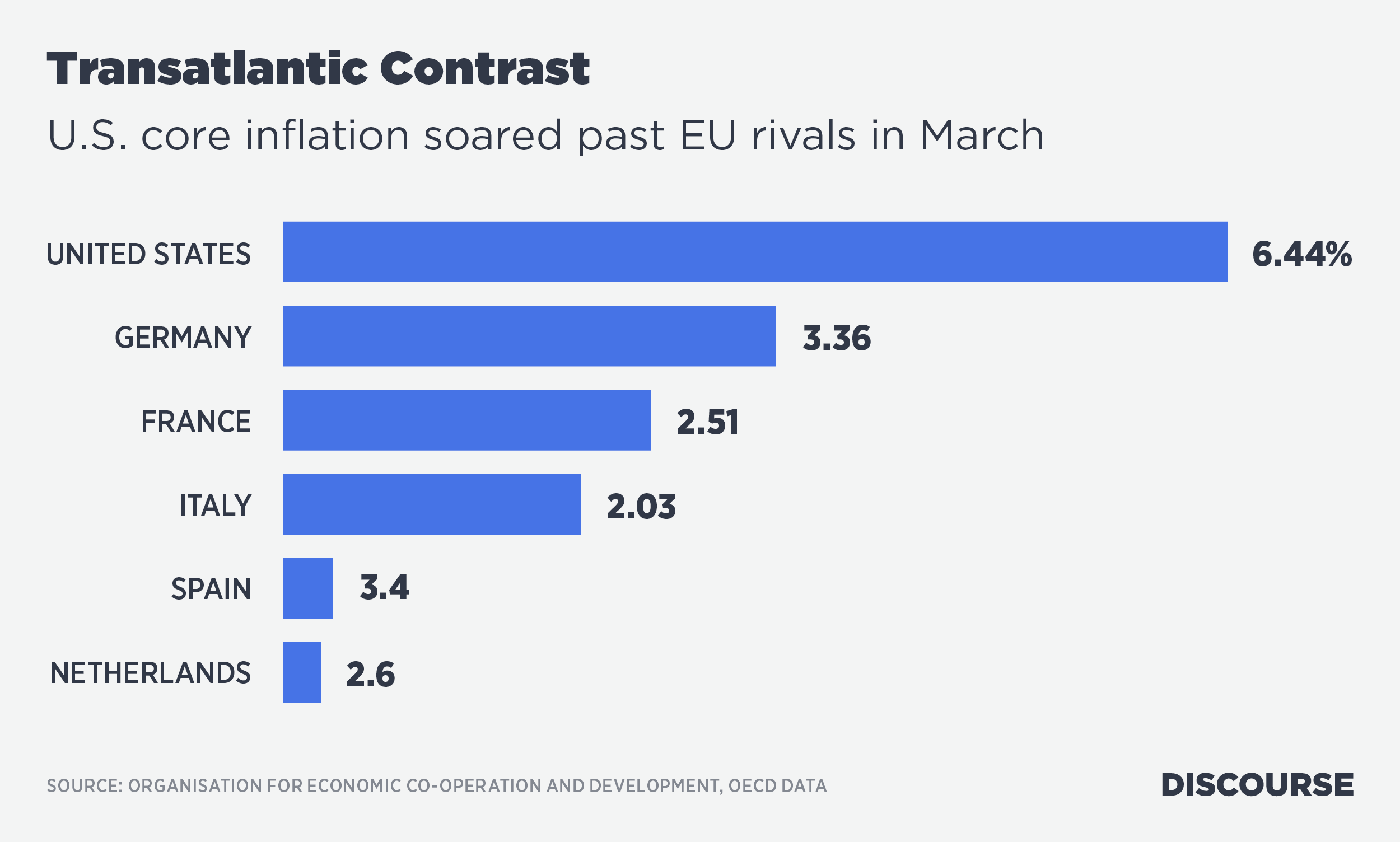

Similarly, if we look at the five largest Euro Area economies, headline inflation is quite elevated, from 4.5% in France to 9.8% in Spain (as of March data). However, comparing core CPI levels of these five economies with that of the United States again shows that core inflation is significantly higher in the U.S. This suggests that Euro Area inflation is largely supply-related, while U.S. inflation is largely demand-driven.

Demand, Not Supply, Is Causing Price Increases

Blaming the 2021-22 U.S. inflation surge mostly on supply chain problems is like blaming a clogged drain hole on an overflowing sink, while ignoring the fact that the tap is still running. Better to turn off the tap before addressing the drainage issue.

There are, of course, ways to make supply chains even more dynamic and resilient, though none of them have been proposed by the president. For example, repealing the Jones Act would reduce costs and alleviate pressures on inland transport, while repealing the Foreign Dredge Act would lower the cost of maintaining U.S. ports, allowing expansions to accommodate more and larger ships.

The Biden administration could remove all punitive tariffs, duties and quotas, which inflate costs and reduce the supply of goods that are essential for meeting growing demand. Recent research by the Peterson Institute finds that reducing tariffs by just 4.2 percentage points could shave 2 percentage points off CPI in the long term. While they’re are at it, the administration could also let in more immigrants to help ease acute labor bottlenecks and end occupational licensing schemes.

While long-term reforms to U.S. supply chains will better align supplies with aggregate demand, policymakers have to stop ignoring the underlying drivers of inflation and excusing the fiscal and monetary doves who will otherwise avoid dealing with the problem at hand. As Harvard economist Jason Furman recently noted, “When considering the economy as a whole, it is implausible that all the individual supply stories would add up to the generalized inflation we have seen. It is far more likely that the increase in demand exceeds what the economy can produce, leading to higher prices.”