The Greatness of Growth

To bring about higher living standards, better health and safety, and more fairness in the American political system, we should unleash economic growth

By Veronique de Rugy

Do you remember when 2016 Republican presidential candidate Jeb Bush campaigned on growing the economy at an annual rate of 4%? Probably not, as his campaign was short-lived. But we also seem to have collectively forgotten that much higher growth rates are not only possible in theory, but they are incredibly desirable too—particularly in the face of anemic growth rates since the early aughts.

Economic growth can lift people out of poverty faster than anything else. But growth also helps with some of the most dysfunctional aspects of our government, especially overgrown debt. Indeed, in a political environment in which doing the right thing—i.e., cutting spending and reforming the drivers of government debt—is unlikely, sustained economic growth would provide a relatively easy and pain-free way to chip away significantly at our $31 trillion federal debt. And if by some miracle politicians did decide finally to cut spending, economic growth would certainly help the proverbial medicine go down more easily.

However, there is an even bigger imperative for promoting growth. The policies required to remove the shackles that have paralyzed the U.S. economy for more than two decades would not only unleash creative forces and innovations, but they would also restore much fairness into a rigged political system.

The Best GDP per Capita Booster, Period

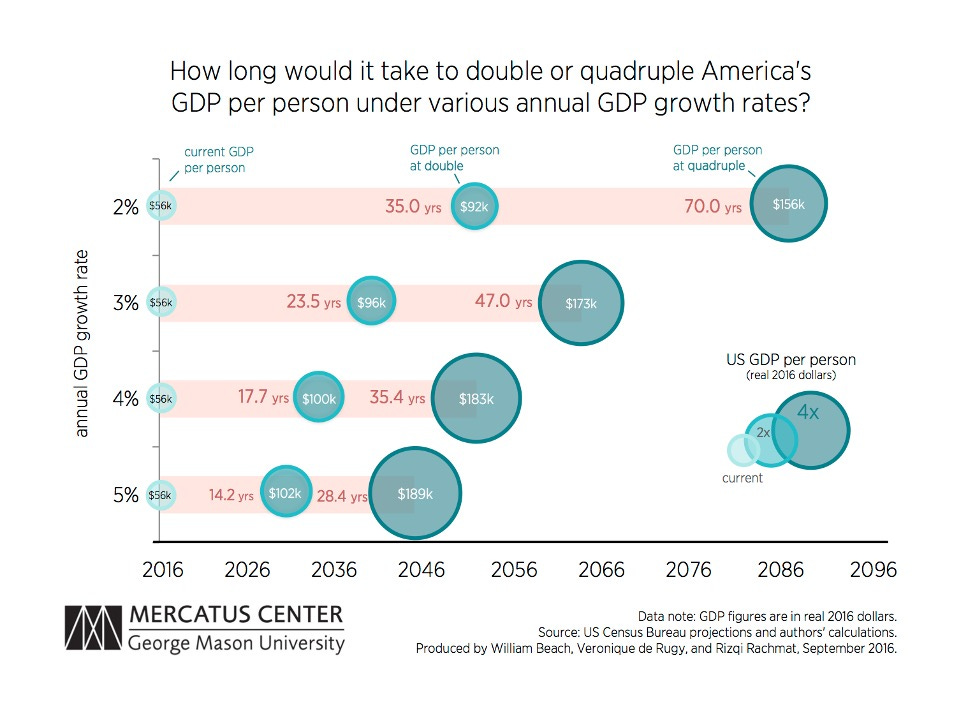

A few years ago, my colleagues William Beach, Rizqi Rachmat and I produced the below chart as a visual reminder of economic growth’s unquestionable and remarkable benefits. It shows that if the economy grows at a long-term, inflation-adjusted 2% annual rate, then it will take 35 years before the size of the economy—measured in per capita GDP—doubles. If instead the economy grows at a sustained average annual rate of 3%, it will double in size in 23.5 years. If the economy grows even faster, at a sustained average annual rate of 4%, such a doubling will take only 17.7 years.

What you can’t see from the chart is that the absence of growth is as painful as its existence is glorious. The economy grew at an average of 3.5% between 1950 and 2000. Since 2000, that rate has slowed to 1.7%. The cost of lower growth is real. John Cochrane does the math for us: “If the U.S. economy had grown at 2% rather than 3.5% since 1950, income per person by 2000 would have been $23,000 not $50,000.”

What policy other than economic growth has the power to double the average American’s living standard in a generation? None. And here’s the cherry on top: All the stuff an advocate anywhere on the political spectrum claims to value—good health, clean environment, safety, families and quality of life—depends on higher growth.

Faster economic growth is likely to engender even greater benefits for the bottom 50% of the income distribution, which contains young people just starting their careers, retirees trying to stretch their fixed incomes with part-time work, and those populations that are caught in intergenerational cycles of poverty. And this is true everywhere in the world. As Harvard University’s Dani Rodrik rightly sums up, “Historically nothing has worked better than economic growth in enabling societies to improve the life chances of their members, including those at the very bottom.”

There are other well-documented material consequences of modern economic growth, such as lower homicide rates, better health outcomes (babies born in the U.S. today are expected to live into their upper 70s, not their upper 30s as in 1860), increased leisure, more and better clothing and shelter, less food insecurity and so on.

‘Growth Is Sublime’ but Politically Difficult

While the material improvements produced by growth are phenomenal, this is not the only reason why Eli Dourado wrote a couple of years back that “economic growth is not only ethical: It is sublime.” Indeed, the real case in favor of economic growth is a moral one. In his criminally underrated 2005 book “The Moral Consequences of Economic Growth,” Harvard professor Benjamin Friedman writes, “Growth is valuable not only for our material improvement but for how it affects our social attitudes and our political institutions—in other words, our society’s moral character, in the term favored by the Enlightenment thinkers from whom so many of our views on openness, tolerance and democracy have sprung.”

Unfortunately, the slowdown of growth increases the risk that we lose ground on political democracy, individual liberty and all those good noneconomic things that we like. That is true even if the absolute level of prosperity remains high. A 1992 paper by Alberto Alesina, Sule Ozler, Nouriel Roubini and Phillip Swagel, for instance, finds that in countries and time periods where growth is significantly lower than otherwise, there is a high propensity for government collapse. In other words, economic growth and political stability are deeply connected.

Given that economic growth is an enormous benefit economically, as well as a moral imperative, my colleague Tyler Cowen argues in his book “Stubborn Attachments” that economic growth, properly understood, should be an essential element of any ethical system that purports to care about universal human well-being. In other words, the benefits are so varied and important that nearly everyone should have a pro-growth program at or near the top of their agenda.

Yet across the board, that isn’t the case. From the radical left, which is now embracing instead a strange “degrowth” agenda, to the New Right pundits and politicians arguing for common-good capitalism—meaning heavy-handed government interference in markets to achieve the outcome they prefer with other people’s money—good old economic growth has fallen into disfavor in recent years.

Another obstacle, maybe even the biggest one, to achieving a maximizing sustainable growth agenda in the U.S. is political. Special interests have convinced politicians to create an inefficient and imbalanced tax code, and they have also demanded a treacherous regime of subsidies, licensing requirements, barriers to market entry and oppressive regulations. These policies have “redistributed” hundreds of billions of dollars to the special interests—I’m thinking of you, seniors, clinging to Social Security and Medicare despite their unsustainable spending growth while being overrepresented in the top income quintile—who certainly aren’t going to relinquish these special favors anytime soon.

According to a recent Gallup poll, just 21% of people believe the country is going in the right direction and 23% approve of the way Congress is handling its job. We are teetering on the edge of a serious recession combined with an interest-payment crisis brought on by the Federal Reserve’s need to rein in the inflation that it created at the prompting of politicians and special interests. While these unpleasant developments could push voters further into the arms of those calling for an even more illiberal regime, it might also prompt voters to open their eyes to the reality that government isn’t a miracle worker and should be reined in.

The Likeliest Path to Fiscal Sustainability

The U.S. is on a fiscally unsustainable path. The debt-to-GDP ratio is around 96% and is projected to grow to 185% within 30 years. While reforming entitlement programs or cutting spending would be the right policies to address this problem, the political chance of legislators implementing these unpopular policies is extremely small. Politicians would be more likely to cut spending, though, if the economy were growing faster and people’s living standards were rising, which would make scaling down government spending less painful.

This means that the most politically feasible way to chip away at our debt is to have higher growth. Now, our debt has reached such high levels that there is no level of growth that can solve the problem entirely. That said, a growing economy can put the country on safer ground.

Using the Congressional Budget Office’s debt ratio and baseline real GDP growth and its average real growth rate of 1.7% over the next 30 years, we can compare this baseline with what would happen to the debt ratio over time if the country suddenly experienced a sustained rate of 3% or 4% growth. The baseline debt ratio reaches 185% after 30 years. Under the 3% growth scenario, debt reaches 124% after 30 years, and with 4% growth debt reaches 93% after 30 years.

In other words, an additional benefit of economic growth is that it helps the government pay down its debt. History shows the effectiveness of this strategy: A strong economy contributed to the most dramatic reduction in the debt-to-GDP ratio after World War II. Robust growth also helped reduce the debt-to-GDP ratio during the years 1994 to 2001.

Good and Bad Ways to Encourage Growth

Some believe that a key to growing the economy is income or wealth redistribution, but this view is a mistake. While redistribution provides temporary relief for some of the poorest, it stunts personal success—not least because receiving the help often requires staying below some level of income. Subsidies or price ceilings do make things cheaper, but they also distort prices. Take the Export-Import Bank, an agency that subsidizes foreign loans to companies buying American goods. The export subsidy shifts capital away from nonsubsidized borrowers—making borrowing rates higher for them—toward the subsidized borrowers, regardless of the merits of each borrower.

The same is true of subsidies meant to lower the cost of buying a home, such as the mortgage interest deduction. The handout allows homeowners to deduct their interest payments from their taxes. This artificially inflates the demand for mortgages, making owning a home more difficult for lower-income buyers. Finally, policies like the expanded child tax credit, especially if it doesn’t require beneficiaries to work, will create some disincentives to work. That will in turn increase child poverty. Decades of economic literature show that this approach tends to backfire and produce quite negative effects that are the opposite of its intentions.

One growth-oriented way to make the income distribution fairer is to get rid of all the programs—including tax favors—that redistribute money to wealthy households (think about the green energy tax credit or the recent push for the expanded child tax credit), well-connected industries (airline and bank bailouts, perks to Boeing and other large companies) and other politically powerful groups, such as public-sector labor unions.

Faster growth would also come from providing more flexibility in prices, wages, employment and the ability to start or dissolve businesses. Simplifying the tax system is a good idea too. Lowering marginal rates reduces disincentives to earn income, while broadening the tax base by removing exemptions and loopholes allows the government to raise revenue as it discourages wasteful lobbying for special tax privileges.

But the single most important move to boost growth is to deregulate. The evidence is overwhelming that deregulation unleashes technological innovations. In his book “Evasive Entrepreneurs and the Future of Governance,” Adam Thierer thoroughly documents that tech innovation is the greatest source of productivity gains and economic growth. For instance, he cites an Obama administration report stating that “technological innovation is linked to three-quarters of the nation’s post-WWII growth rate” and “innovation in capital goods is the primary driver of increase in real wages.” In addition, 75% of the differences in income across countries can be explained by innovation-driven productivity differentials.

How much does such regulation affect growth? John Dawson and John Seater published a widely cited 2013 research paper in the Journal of Economic Growth that finds that GDP has been reduced by a surprising $39 trillion over the period 1949 through 2005 due to regulation. They estimate that this loss amounted to $129,300 per person by 2005. This finding was echoed by World Bank researchers, who found that a 10% increase in regulatory burden is associated with a reduction of 0.5 percent in the overall economic growth rate annually. That loss translates into thousands of dollars in lost income per person.

More recently, my colleague Patrick McLaughlin and his co-authors looked at the effect on growth of regulatory policy changes that would have frozen the accumulation of regulations at the level observed in 1980. They find that the economy would have grown 0.8 percent faster in the simulation annually.

If you wonder how this affects your daily life, let’s look at housing as a concrete example. Americans spend 30% of their income on housing. It’s the biggest item in their budgets. Politicians have sunk hundreds of billions of dollars into building affordable housing over the years, only to face diminished housing supplies and higher prices. The good news is that there is a large literature on the above and beyond costs imposed on families. There is a similarly large literature on the benefits of housing deregulation. The mechanism is simple enough: Fewer regulations mean more supply; more supply means lower prices; and lower prices allow workers in low-productivity regions to move to high-productivity regions. This geographic movement of workers will itself increase economic growth nationwide.

The second-biggest item in the average American household’s budget is transportation expenses. Politicians claim that the way to reduce transportation costs is to sink a lot of government money into infrastructure. They believe that more public money in infrastructure will also generate growth. Economic evidence, however, shows that public-investment infrastructure is a bad bet.

What would actually make a big difference is loads of private money invested in infrastructure and transportation innovation. Unfortunately, this task is much harder than it should be, as is known by any enterprising innovator who wants to lower transportation costs by building more roads with better materials to reduce road congestion, or by building high-speed underground rail projects going from Baltimore to Washington. Entrepreneurs who want to innovate in the area of transportation find themselves mired in red tape, including environmental-review requirements that create costly delays.

The third-biggest budget item faced by American households is food. The government massively regulates the food industry, without making it any safer, and spends over $140 billion a year subsidizing food via food stamps, on top of a few billion dollars in farm subsidies. Of course, plenty of farm subsidies and tariffs are directly meant to increase the cost of food, not reduce it. All that government intervention hasn’t made food any more affordable. A change in the way we produce food could, however, make a big difference. This may look like growing meat in a lab, vertical farming or some other technology. Any such innovation would not only expand supply and lower the cost of food, but it would also grow the economy.

However, innovation-inhibiting regulation may be the most damaging to a sector on which all the others depend: energy. This is a big deal since so much of the degrowth movement is grounded in the fear of running out of resources—and energy is foremost among them. The answer to such fears, of course, should be the quest for energy abundance, not degrowth. That would require knocking out the barriers to innovation that exist today—including, but not limited to, energy restrictions imposed through heavy-handed laws and regulations that not only obstruct exploration for more oil and gas, but also raise the costs of developing geothermal, solar and wind energy sources. More energy innovation, and the economic growth that will flow from it, require ending all energy subsidies, fuel economy standards, Tesla tax credits and other price-distorting measures.

We could go down the list of American households’ budget categories and find that we would be better off with fewer rules, more innovation, more supply and lower prices. The economic bang for our buck could be huge. Even if removing all these rules improves efficiency by only 10% or so, we will get more growth, more labor, more productivity, more innovation and more new businesses. More growth also means more revenue and a smaller deficit, especially if Washington’s drunken sailors can keep their hands off the proceeds. Maybe we get to 4% per capita GDP growth, and maybe we don’t—but we sure have a better chance by pursuing growth than by continuing to throw public money and regulations at problems without ever making a difference.